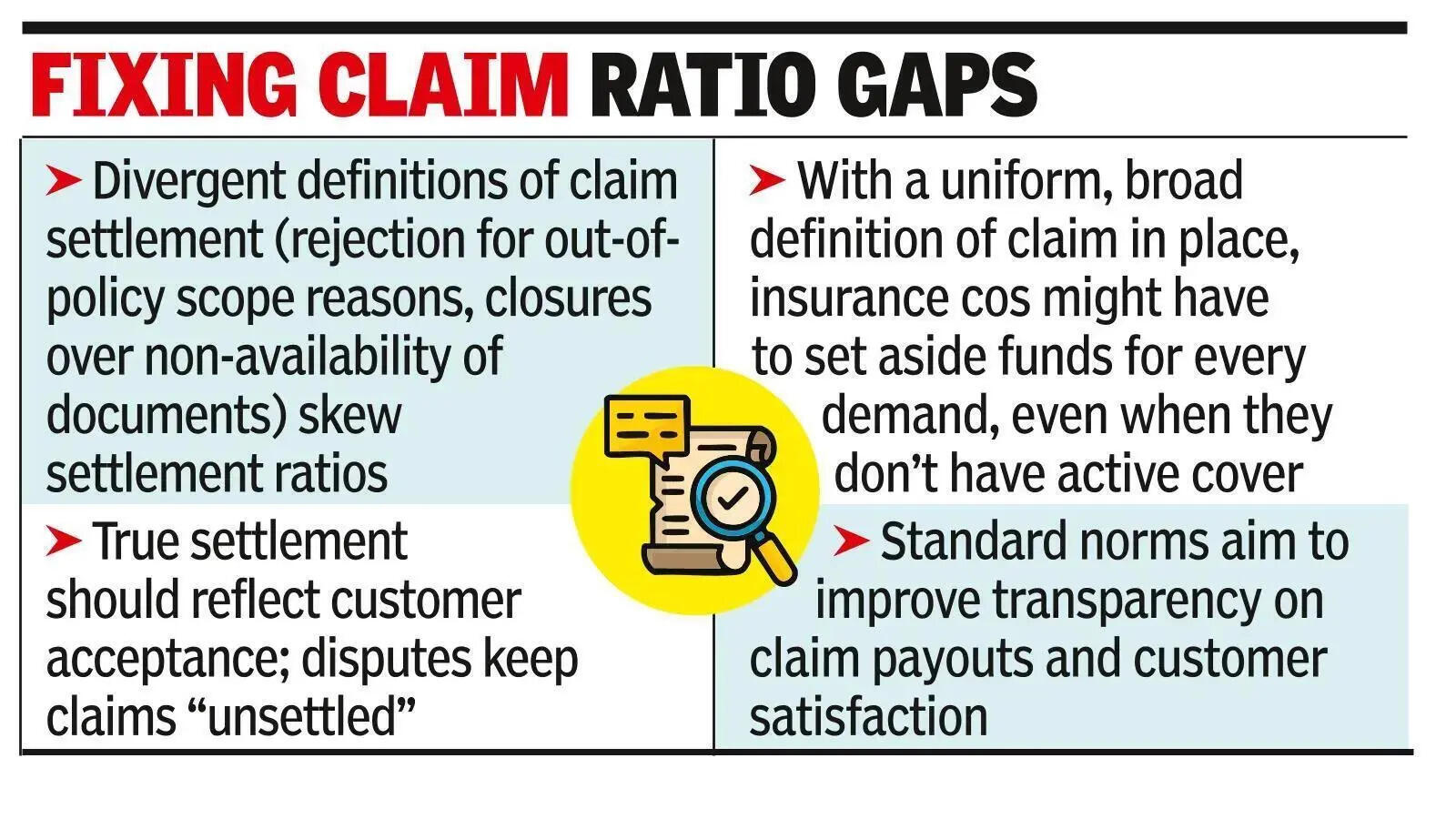

MUMBAI: IRDAI has asked the non-life industry to come up with a standard definition of claim and a uniform definition of claim settlement ratio for various lines of business. This followed different companies using different definitions for determining claim settlement ratio, a key metric that is an indicator of companies’ financial health and customer satisfaction.Some companies register a claim at the first instance while others do so after establishing liability under a policy. While for the layman a ‘settled claim’ is one where the insurance company has paid to their satisfaction, some insurance companies treat claims closed by them for non-availability of documents or claims rejected for not coming within the scope of the policy as settled claims. While this helps the numbers add up, it gives a uneven picture of how many customers are getting what they claimed.“The general insurance council has submitted their views on standard definition of claim and uniform approach to define claim settlement ratio for various lines of business to IRDAI as required by them. This is to ensure that a clear picture emerges in regard to a company’s claim settlement standards without variation in different approaches by each company at various steps,” said an industry source.

” In simple reality a claim can be treated as settled only if the client confirms that it is settled. Till that is done, the claim remains pending / disputed ” said KK Srinivasan, former member non-life at IRDAI. He added that if a claim is repudiated by an insurance company, it can be disputed legally within 3 years of repudiation and will remain disputed till the court disposes it off. “Once a court admits the repudiation or dispute for hearing, it has to be treated as unsettled till the court or forum disposes it off and the order of the court is complied with,” he added.While companies ask claimants to give a discharge voucher saying they accept the full and final settlement, there are many claims where the customer is not satisfied. The definition of a claim is essential to determining the incurred claims ratio which determines underwriting profits. A broad definition of a claim would mean that insurers would have to set aside funds for every demand made from them even when they do not have active cover.“The claim settlement ratio has to be seen over a period of time. It is possible for a company to have a claim settlement ratio of over 100 if it settles all claims and the claims pending from the previous year,” said the former CEO of a non-life company.

{kind=link}